The Terra blockchain was launched in 2018 by a Stanford-educated entrepreneur named Do Kwon and his company Terraform Labs. Its central product was a stablecoin called TerraUSD — ticker UST — which was designed to maintain a one-dollar peg through what Kwon and his colleagues described as an algorithmic mechanism. Unlike traditional stablecoins such as USDC or Tether, which maintained their dollar pegs by holding actual dollars or dollar-equivalent assets in reserve, UST maintained its peg through a coupled relationship with a free-floating cryptocurrency called LUNA. When UST traded above one dollar, users could mint new UST by burning a dollar’s worth of LUNA. When UST traded below a dollar, users could burn UST to mint a dollar’s worth of LUNA. The arbitrage opportunity, in theory, kept the peg intact. The mechanism, in theory, did not require any external dollar reserves at all.

The mechanism’s central weakness — that the peg’s defense depended on LUNA’s market capitalization remaining substantially larger than UST’s — was widely noted by skeptical observers from at least 2020 onward. Kwon’s response to skeptics, conducted primarily on Twitter and characterized by an aggressive and personal style of debate, was to bet against them, sometimes with stakes in the millions of dollars. The bets attracted attention. The attention attracted users. By early 2022, UST had a market capitalization of approximately $18 billion, was the third-largest stablecoin in cryptocurrency, and was earning users approximately twenty percent annual yield through a Terraform-controlled lending protocol called Anchor. Where the yield came from was a question that received less public attention than it deserved.

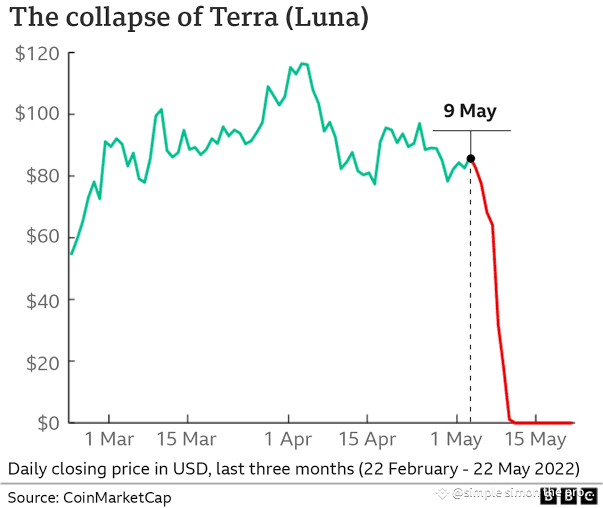

The collapse began on May 9, 2022, with a series of large coordinated withdrawals from Anchor and the simultaneous selling of UST against the peg on multiple exchanges. The peg slipped. UST fell to ninety-eight cents, then ninety-five, then eighty. The algorithmic mechanism activated as designed: users burned UST to mint LUNA, expanding LUNA’s supply rapidly in an attempt to absorb the selling pressure. The expansion did not absorb the selling pressure. It accelerated it. As LUNA’s price fell, more LUNA had to be minted to absorb each additional dollar of UST sales. Within forty-eight hours, LUNA’s supply had increased from approximately 350 million tokens to approximately 6.5 trillion. Its price fell from $80 to fractions of a cent. UST broke definitively below ten cents. The two assets, which had collectively been worth approximately $60 billion on the day before the collapse began, were worth less than $2 billion by May 13. The mechanism, when stress-tested by the market, had not stabilized the peg. It had vaporized both sides of the trade.

The contagion was substantial and not contained to Terra’s direct holders. The Singapore-based hedge fund Three Arrows Capital, which had built a significant LUNA position, became insolvent in June 2022 and triggered a cascade of failures across cryptocurrency lenders that included Celsius, Voyager Digital, BlockFi, and Genesis. By the end of 2022, approximately $200 billion in cryptocurrency-related lending capacity had been wiped out. The FTX collapse in November of the same year, while operationally distinct, was substantially accelerated by the contagion that began with Terra. Kwon was indicted in the United States and South Korea on multiple counts of fraud, securities violations, and market manipulation. He was arrested in Montenegro in March 2023, extradited to the United States in December 2024, and as of mid-2025 awaits trial in the Southern District of New York.

The cultural significance of Terra’s collapse, distinct from its financial dimensions, was that it demonstrated the failure mode the bitcoin maxi community had been predicting since at least 2017: that crypto, in its broader and non-bitcoin-specific sense, contained mechanisms whose stability depended on continuous market confidence and which would unwind catastrophically when that confidence faltered. The bitcoin protocol, by contrast, had not changed. Its supply schedule was unchanged. Its consensus mechanism was unchanged. Its monetary properties were unchanged. The maxi argument that bitcoin was structurally distinct from the rest of the cryptocurrency category — an argument that had previously been the subject of considerable mockery from outside the maxi community — found in Terra’s collapse a kind of unforced empirical confirmation. The phrase bitcoin not crypto circulated more widely in 2022 than it had in any prior year. Most of those circulating it could now point to a specific forty-billion-dollar example of why the distinction mattered.